It’s a race to the bottom in oil price forecasting. What a strange world. The Middle East is on fire. The Russians and the Americans are bombing ISIS oil conveys. And oil is in free fall.

Goldman Sachs led off with a prediction that the global supply glut could send West Texas Intermediate and Brent Crude prices below US$20/barrel. It’s a producer price war for global market share. The Saudis should win because their cost of production is lower than everyone else. But the question is how low the price will go before some producers are squeezed out.

Of course you can sell a commodity at below the cost of production if you’re willing to ignore profit and loss. National oil companies – oil companies belonging to the state rather than investors – are run as tools of national economic and security policy. I’m talking about PEMEX in Mexico, Petrobras in Brazil, Statoil in Norway, and of course Saudi Aramco.

But the price war in the oil market is going to claim some victims soon enough. And I’m not talking about the tar sands and shale gas producers in North America. Take a look at the chart below. The current $40 level was a ceiling for the oil price in 2000 and 2003. But it was a floor in 2009. And now?

At $20/barrel, oil is telling you that there’s little global GDP growth. Only stockpiling is driving real demand growth. This is the great zombie/low interest rate/Japan-style era of global depression.

Conversely, as a trade, well, you could take your chances betting on a $40 floor. You’d have to argue that investment demand (financial demand) and a geopolitical ‘fear premium’ would support oil from here. That’s the case I made on the Capital and Conflict podcast yesterday.

Draghi goes boom

What do you reckon the best trade of 2016 will be? Will it be the divergence of US and eurozone interest rates? As the Fed talks a tough game on ‘normalising’ in December, Mario Draghi is headed in the opposite direction, at least rhetorically.

Yesterday he said this: “If we decide that the current trajectory of our policy is not sufficient to achieve that objective, we will do what we must to raise inflation as quickly as possible. In making our assessment of the risks to price stability, we will not ignore the fact that inflation has already been low for some time.”

‘That objective, by the way, is 2%. For reasons not yet sufficiently explored in this space, central bankers target 2% inflation as a sign that ‘loose’ monetary policy is doing its job. It means all that easy credit is translating into borrowing and spending. That activity raises the temperature in the economy, as indicated by inflation.

But really, come on. In order to achieve price stability we must inflate! Can you see how it makes no sense? There are two major contributions to the low level of official inflation. First is the aforementioned oil price. It’s passed through, at least in theory, in the form of lower energy prices throughout the entire economy.

And then there is the ‘output’ gap in the Western world. Economies grow ‘below trend’ when productivity is lower than it should be. It means a given amount of capital and labour is ‘underperforming’, or ‘not living up to its potential’ as a teacher may have told you when you were learning maths and handwriting in school.

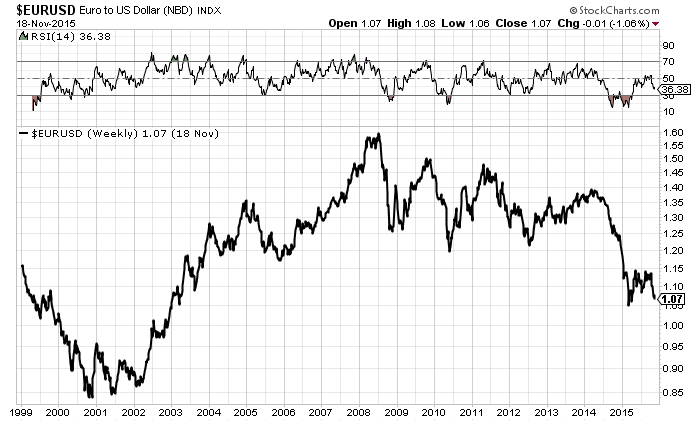

The reasons for the ‘output gap’ in the Western world are legion, and beyond the scope of today’s article. Suffice to say that the ‘solution’ of the European Central Bank (ECB) will be more of the usual: going negative on deposit rates and expanding quantitative easing (QE). I will leave aside the implication of negative rates for now. What will more QE mean? Have a look at the chart below.

If US and EU rates diverge, is it possible the euro could challenge its all-time lows against the dollar? Well, yes. Anything is possible. A stronger dollar would be accompanied by lower oil (Goldman could be right). That’s one scenario.

And there’s the ‘existential’ question. It’s extreme to suggest Europe’s migration and security crisis could pose not just a threat to ‘ever closer union’ but the end of the Union. At least for Britain, in the form of Brexit. But keep it in mind for 2016.

If form holds, some sort of muddle-through solution will keep Britain in Europe. But the European Union is facing its most serious political, economic, and monetary challenges in decades. It’s still a productive economic zone with 500 million relatively affluent consumers and world-class manufacturing and financial services. But the monster that is the common currency? That could be in for a rocky future. Charlie Morris will have more on that next week in the cover story for MoneyWeek. Until then!

Category: Market updates