I have some bad news.

That’s if you like gold, at least. If you hate gold, this is probably great news; a ray of sunshine to brighten your day.

And if you’re neutral about gold, perhaps this’ll just add some colour to your view of investor sentiment.

But anyhow, let me start with some context.

I like to keep in touch with my old schoolmates back in Aberdeen. Whenever I’m back up there, I endeavour to meet up with them and catch up over several pints. But that’s usually just around Christmas or the BrewDog AGM, so most of the time everybody just keeps up to speed with one another over WhatsApp. We have a group chat (effectively a shared digital shouting area) into which everybody can banter and dump their opinions.

None of these fellas work in the financial industry, but several enjoy gambling (which is close enough) and a few try their hand at playing the stockmarket. One of the key indicators which I noted but failed to act upon during the 2017 crypto boom was when my mates were asking me which cryptocurrencies they should buy – that was a clear sign that it was time to get out.

When the general public gets excited about an investment trend or idea, they’re normally too late: the smart money has already got in early, and the largest investment returns have already been made.

When the everyman is buying stocks that have made headline news and telling his friends they should do the same, that’s often (sadly) a sign that you should sell. It indicates that we are near a market top, or that the asset in question is now in bubble territory.

With that in mind, I regret to inform you that my friends have begun talking about one of my favourite assets of all – gold – as a speculative asset to make a quick buck.

I grimly gazed on at my phone screen as one schoolmate, who had become interested in crypto in Christmas 2017, announced that he had just invested in a physical gold ETF. Justifying his bullishness, he claimed that gold was up 125% this year – a statement true and then some in a country like Venezuela, though not so much here in Blighty, where it’s up 27% YTD.

I shrugged off the significance of this fella’s interest in crypto back in 2017, to my loss (How I lost thousands in one of the greatest bull markets in history – 3 March). Should I dismiss his interest now?

I’ll flesh out my thoughts on whether gold has become overcooked in tomorrow’s note. In the meantime, if you have any similar tales of friends or family who were previously not interested in suddenly catching the gold “bug” recently, I’d love to hear them: boaz@southbankresearch.com.

How significant was Brown’s Bottom to Britain?

When speaking of gold and timing the market badly, one immediately thinks of Gordon Brown. His sale of Britain’s gold reserves at the bottom of the market has gained infamy as a fiscal error, earning the title of “Brown’s Bottom”.

Charlie Morris over at The Fleet Street Letter Wealth Builder was recently asked by one of his subscribers on just how significant this act really was. I’ll leave you today with the question asked, and his response. In short: if you think the Treasury was making a mistake, then just take a look at what it’s doing now…

In the post box…

Just a small thought: My impression from the media when Gordon Brown sold our country’s Gold was that we had sold all of it. Recently I read an article that said he had sold half of it. This came in a piece of all the countries placings that hold Gold Bullion and the UK came 19th (shameful). Now I read that you say Brown sold a third of our Gold. How does a member of the public come to know the exact truth at anytime?

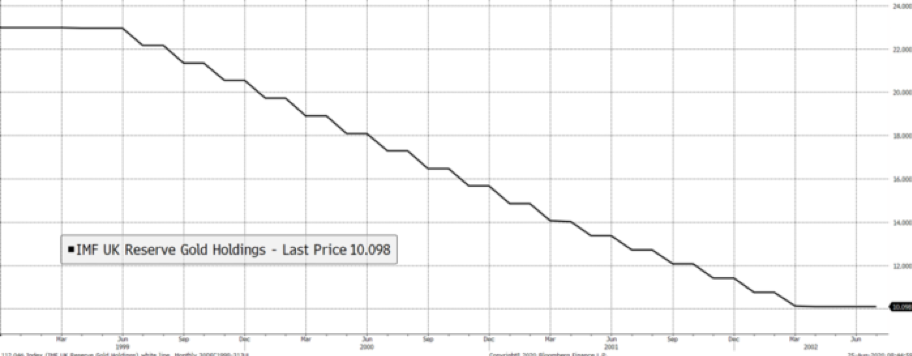

Here is the answer from HM Treasury. It tells you that 395 tonnes were sold between 1999 and 2002 at an average price of $274.92 per ounce with total proceeds of $3.5 billion.

The drop in reserves can be seen here measured in million ounces. The UK went from 23 million ounces to around 10 million ounces.

UK gold reserves

Source: Bloomberg – Bank of England gold reserves in million ounces 1999 to 2002

With one metric tonne making up 32,150 troy ounces, the current value of the gold sold is:

395 tonnes x 32,150 ounces x $1,930 per ounce = $24.5 billion.

It sounds like a lot, and probably is. But it was less than July’s government deficit of £26.7 billion. Just putting it into perspective.

One more thing please: Has the UK made a profit of selling our Gold in comparison to what was purchased in its place? Thanks for your help.

Yes and no. I imagine that gold was held for decades, and probably centuries. Gold doesn’t make much (or anything) in real terms over very long periods of time, yet it makes lots under certain conditions such as we are seeing this century.

The proceeds of the sale would be largely profit in nominal terms as the prevailing gold price pre-WW1 was around $20 (1920), so that’s a healthy profit, but considering inflation and so on, not a very good one.

Recall that the pound wasn’t quite how it was described by Banks in Mary Poppins, “the British Pound is the envy of the world”, in the 1970s. However you look at it, it wasn’t a very good trade, but not nearly as significant as made out. As I said, less that July’s deficit spending in a nation with £2 trillion of debt, it barely moves the dial…

Until tomorrow,

Boaz Shoshan

Editor, Capital & Conflict

PS Incidentally, while gold has become speculative asset numero uno amongst my friends, I haven’t heard anybody talk about crypto recently – despite some of the wild action in that market which we’ve been detailing in these letters. There are many folks who still think the entire thing is a scam however – and their complaints have been driving my colleague Sam Volkering to distraction over at our sister publication, Exponential Investor. In today’s note, he tries to clear the water and make a distinction between a tulip, a Ponzi – and a bitcoin.

Category: Investing in Gold