“Gleich funkt es,” my German family always said as their final warning.

It roughly translates to, “Any moment now, sparks are gonna fly.”

Youngins on the receiving end of that comment got their act together real quick.

Have you noticed the sparks flying in the financial news? Not the ones about the FTSE 100 hitting an all-time high. I’m talking about the other FTSE. The Italian MIB index. It’s down 5% in a week. Italian bank stocks are down 10%.

And that’s just the warning. Gleich funkt es.

Recently, the media has cottoned on. Countless commentators are pointing out how serious the situation could get. But they’re late.

The fuse was lit one month ago

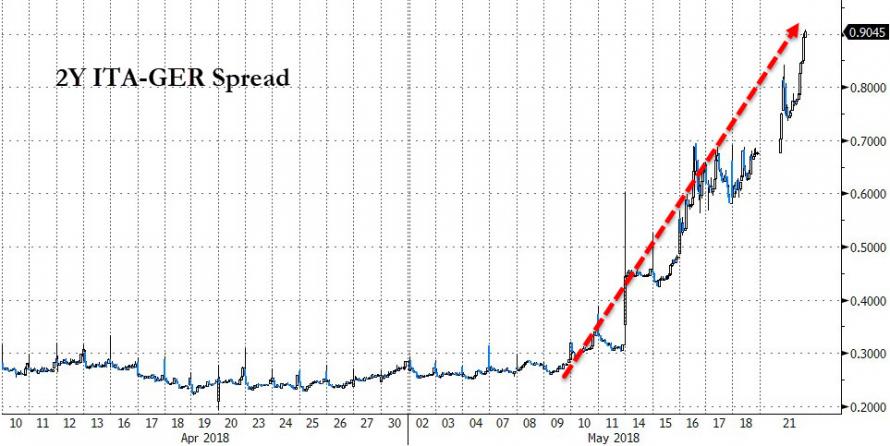

On 25 April, Zero Hour Alert published its report on the coming financial crisis in Italy. The spread between German and Italian ten-year bonds bottomed out that day. And held steady the next.

Then this happened:

Source: Zero Hedge

Source: Zero Hedge

Why focus on the spread? Because it’s like adjusting the wave height for the tide. The gap between German and Italian bonds gives you the risk of Italy specifically.

Reuters reports that the Italy-Spain yield gap is at its widest in six years – back to 2012 and the height of the European sovereign debt crisis. In other words, Italy’s bond market specifically is decoupling.

The problem is no longer a distant concern. Italy’s two-year bonds are caught up in the spike too now. The yield has gone from -0.3% to over 0.26% in three weeks. The spike above German bonds is even more pronounced:

Source: Zero Hedge

Source: Zero Hedge

Just days after the rout in two-year bonds began, the Italian bank stocks began to sink next. The FTSE Italia Banche index is down over 10% since 15 May.

The fuse was lit back in April. It’s been hissing and sparkling towards the powder keg in Italian bonds, banks, politics and the very heart of the euro.

Even the mainstream media has cottoned on.

Gleich funkt es.

So let’s review what’s really going on.

Finances, maths and politics are never a good mix

The leader of the Lega party called the market’s reaction to his governing coalition “blackmail”.

This personification of “the market” as a vicious villain is something that’ll come flying out of Italy thick and fast in coming weeks. In reality, the selloffs are driven by fear, not some sort of maliciousness.

The rhetoric also distracts from the simple mathematical implication. Italy must refinance its debt at the higher rates. And with debt to GDP over 100%, each tick up in rates translates to the same tick up in the proportion of GDP that’ll go to interest expense over time.

Markets cannot be shrugged off. Especially if you want to finance even more spending. As the new government does.

Ratings agency Fitch piled on the pressure yesterday by warning the new Italian government about its fiscal plans. The costs would be vast, the revenues minor, the deficit will blow out by another 6% of GDP according to Citigroup, and the “willingness to push back against EU fiscal rules … increases the risk both of a further rise in public debt and of a destabilising reaction by economic actors and in financial markets”.

A party leader inside the EU parliament even spoke up, saying “This could provoke another eurozone crisis.” Given that it’s the EU which the new Italian government has singled out as its enemy, this is an admission straight from the horse’s mouth.

Commentators in the media are still unsure what’s caused the sudden change. Is it the proposed budget policies of the new coalition? Perhaps their stance to challenge the EU’s fiscal rules? Or the introduction of the mini-BOT currency and its threat to replace the euro?

The answer is obviously a combination of all four. They’re deeply interconnected. And they’re coming to a head thanks to the 4 March elections.

A manifesto of threats and promises

The coalition set to govern Italy has released its manifesto. The aim is to blackmail the EU into waiving the fiscal rules as a concession to keep Italy in the euro.

If the EU does not comply, Italy’s government threatens to raise the stakes in several ways. These were clearly signalled when an early draft of the manifesto was leaked to the press. The governing parties were quick to say that this document was an old and out-of-date version of the manifesto.

It wasn’t. Think of that leaked document as a warning. They’ve detailed the consequences if they don’t get their way with the EU. These are, possibly in the right order:

- Issue mini-BOTs as a parallel currency to pay off government bills without technically borrowing money.

- Unleash hundreds of thousands of immigrants.

- Demand European Central Bank (ECB) cancels the Italian debt it holds.

- Demanding a credible euro exit framework for eurozone nations.

- Holding a referendum on the euro.

Each policy is like a card to be played against the EU.

The trump card remains hidden for now. It is unilateral action – a default and leaving the euro.

These two are synonymous. Leaving the euro would trigger a default for Italy, as it can no longer pay euro-denominated debt. Especially when its new currency tumbles to make the country competitive again.

Not leaving the euro, but breaching the eurozone’s rules, would pressure northern states badly politically. But given the choice between an Italian default and a trashing of the euro’s rules and values, it’s not clear what the ECB and its members will chose.

Meanwhile, the Italians have found a different avenue to the same effect. Their mini-BOT currency would allow them to ease fiscal and monetary pressure while sticking it to the ECB and EU.

John Dizard explained this is only a short-term solution. In the Financial Times he laid out where it leads: “If mini-BoTs are introduced on a large scale, political strains would eventually force either Italy or Germany out of the euro. Having done its damage, the mini-BoT scheme would ultimately be wound up.”

Amidst all this, Italy’s economy is hardly improving. Banking expert and investment adviser Christopher Whelan returned to the US after a trip to Europe and summarised his findings on his blog Institutional Risk Analyst:

Italian banks, for example, admit to bad loans equal to 14.5 percent of total loans. Double that number to capture the economic reality under so-called international accounting rules. Italian banks have packaged and securitized non-performing loans (NPLs) to sell them to investors, supported by Italian government guarantees on senior tranches. These NPL deals are said to be popular with foreign hedge funds, yet this explicit state bailout of the banks illustrates the core fiscal problem facing Italy.

It’s another fudge, just like the mini-BOT. A broke country’s broke government backing its broke banking system with a guarantee.

Now that interest rates are surging, the problem will grow dramatically.

Whelan, also a veteran of central banking, believes it’s the leaked manifesto’s demand for the ECB to cancel Italy’s debt bought under quantitative easing (QE) policies that’s particularly interesting:

The Italian evolution suggests that Ben Bernanke, Mario Draghi and their counterparts in Japan, by embracing mass purchases of securities via Quantitative Easing, have opened Pandora’s Box when it comes to sovereign debt forgiveness.

If the populists turn to the printing presses, there will be trouble.

Historically, Italy has leaned on the currency to absorb ridiculous policies like its proposed budget. It shouldn’t be a surprise that the same thing is happening again. Especially when it’s the rest of Europe that bears the weight.

So perhaps it’s the rest of Europe that will unleash Italy. Back to Whalen:

With the UK already headed for the door, the latest political developments in Italy may presage the end of the EU as it stands today. How the Germans and other euro nations deal with the new government in Italy will tell the tale.

Former foreign secretary William Hague explained in the Telegraph how the incentives of Italian politics are set up for a clash:

Disappointment and anger can therefore be directed, not against a new ministry in Rome, but at Brussels and Berlin. It will be the EU that will be preventing Italians from receiving the benefits for which they voted – the very same EU that promised so much help with the huge flow of migrants across the Mediterranean and has then done very little. If the new political leaders want to trigger the bust-up that could lead to Italy leaving the euro, as so much earlier rhetoric from them has suggested they do, the stage will be perfectly set for it.

It seems everyone is now on board with a crisis in Italy.

But what do you care?

How the UK fits in

It’s not just Italy that is nearing a bust. Turkey’s debt and currency crisis is escalating too. Argentina is working with the International Monetary Fund to prevent any further trouble.

The widening gap between these peripheral crises and the key major economies has to close eventually. And it’s the major economies that are looking vulnerable.

And none more so than the UK, especially if it’s a financial crisis specifically. Our economy is a financial centre. That’s why our economy fared second worst during the 2008 financial crisis.

We’ll be in for another economic and financial crash if Italy goes under.

So what should you do? Find out here.

Until next time,

Nick Hubble

Capital & Conflict

Related Articles:

- Opt out of the blunder from Down Under

- Is Italy the weakest point?

- Why the European sovereign debt crisis is back

Category: The End of Europe