“… as of today, the doom loop is very big and very much alive.”

Lorenzo Codogno and Mara Monti – The London School of Economics

Hanging in the Louvre in Paris is a work of art that has provoked debate and courted controversy ever since the oil dried on the canvas centuries ago.

It depicts a group of shepherds inspecting a massive stone tomb. One turns in dismay, pointing to an inscription on the stone. Et in Arcadia ego, it declares – “I too lived in Arcadia”, or “I too am in Arcadia”.

Some conspiracy theorists have claimed that the phrase is actually intended as an anagram of “I! Tego arcana dei” – “Behold! I keep God’s secrets”…

A more common interpretation is that death awaits everybody, even those in paradise (Arcadia) – that all good things must come to an end.

All things must come to an end eventually – even in financial markets.

Nick Hubble first warned that death was coming to the Italian bond market in April. Markets and the mainstream media are slowly beginning to recognise that the illusion paradise created by the European Central Bank (ECB) can’t last forever.

Trouble in paradise: the doom loop

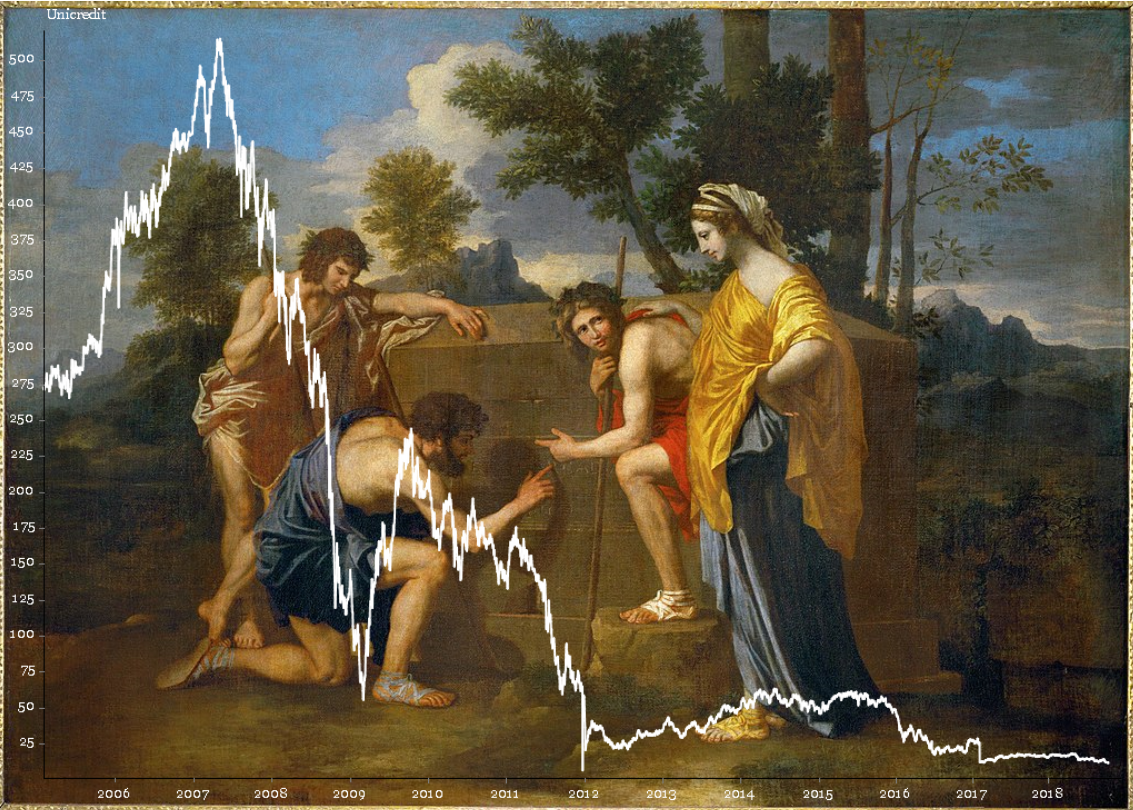

If you’d like to see a more modern depiction of what death arriving in paradise looks like, you need only look at the price action of an Italian bank. This is Unicredit, Italy’s largest:

(Click to enlarge)

(Click to enlarge)

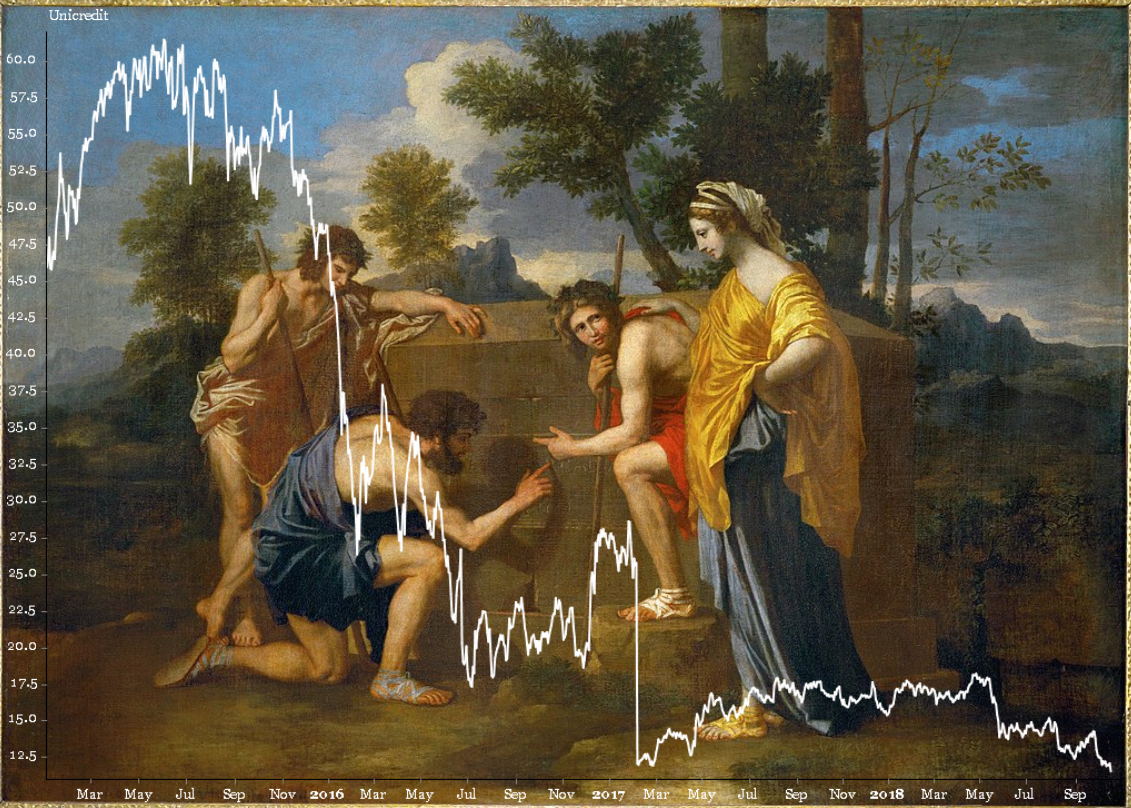

The chart above is a little deceptive as it makes it appear that Unicredit’s stock price has flatlined in recent years. Take a more recent view below, and you’ll see that the extent to which Unicredit has been bludgeoned by the market:

(Click to enlarge)

(Click to enlarge)

Italian banks have been in deep water ever since the financial crisis. Their “non-performing loans” (NPLs, debts that will not be repaid) have weighed them down, lying toxic on their balance sheets.

They’ve managed to package them up and sell a fair amount of them off in recent years (good luck to whoever bought them), however the total amount of NPLs within the Italian banking system still stood at €127.5 billion in July, and it’s not likely they’ve managed to sell much more since then, given the chaos that has followed.

But there’s something much more deadly awaiting the Italian banks. While they were selling off their bad debts… they were buying “safe” Italian government debt hand over fist. Italian government debt that is losing value by the day.

Italian banks now own €381 billion in Italian government bonds, which are dropping in price as investors recognise the risk of the Italian government being unable to pay its debts. The capital of the Italian banks is being indirectly eroded by their own government. Their solvency is being threatened not just by their bad debts – but by the “safe” debts to the government that were supposed to be risk free.

It’s a “doom loop”: collapsing confidence in the Italian government leads to a collapse in confidence in Italian banks, which leads to a further decline in confidence in the Italian government as it’ll then have a banking crisis on its hands on top of everything else.

Markets reflect this reality in the price of insurance for Italian bank and government debt, which is rising in tandem. The chart below, courtesy of Holger Zschaepitz, illustrates how the risk of a default by the Italian government and the Italian banks are moving in tandem:

The ECB created an illusion of peace by propping the Italian bond market up (hence the rally in Unicredit after 2011) but its bond purchases have been declining, and halved at the beginning of this month. Considering the losses sustained in Italian bonds already, when the ECB stops buying Italian bonds altogether (scheduled for the end of the year), Italian banks (not to mention the government) will be in even more trouble.

For all the illusions cast by the ECB, the reality of The Italian Problem will be not be denied. Et in Arcadia ego.

We’re taking our Italy warning webinar offline this weekend. If you’ve not watched it yet, I recommend you do so now.

Have a good weekend,

Boaz Shoshan

Editor, Southbank Investment Research

PS If you’re interested in a radical approach to receiving regular income (almost like dividends, just more regular), then Eoin Treacy has a proposition for you – click here to find out more.

Category: The End of Europe