The men labelled by the Italian deputy prime minister as “the gentlemen of the spread” are roughing him up.

Who are these “gentlemen of the spread”? In short, they’re investors selling Italian debt, and buying German debt instead. The buying and selling has led to the market demanding far less in interest payments from Germany than Italy – a difference, or “spread” between safety and danger.

The Italian deputy PM, Matteo Salvini, said earlier this week that he was “absolutely sure” that this spread would not grow to 4%. A challenge that the “gentlemen” are willing to take him up on. At the time of writing, the spread has zoomed to 3.05%, and still has wind in its sails:

Source: Bloomberg

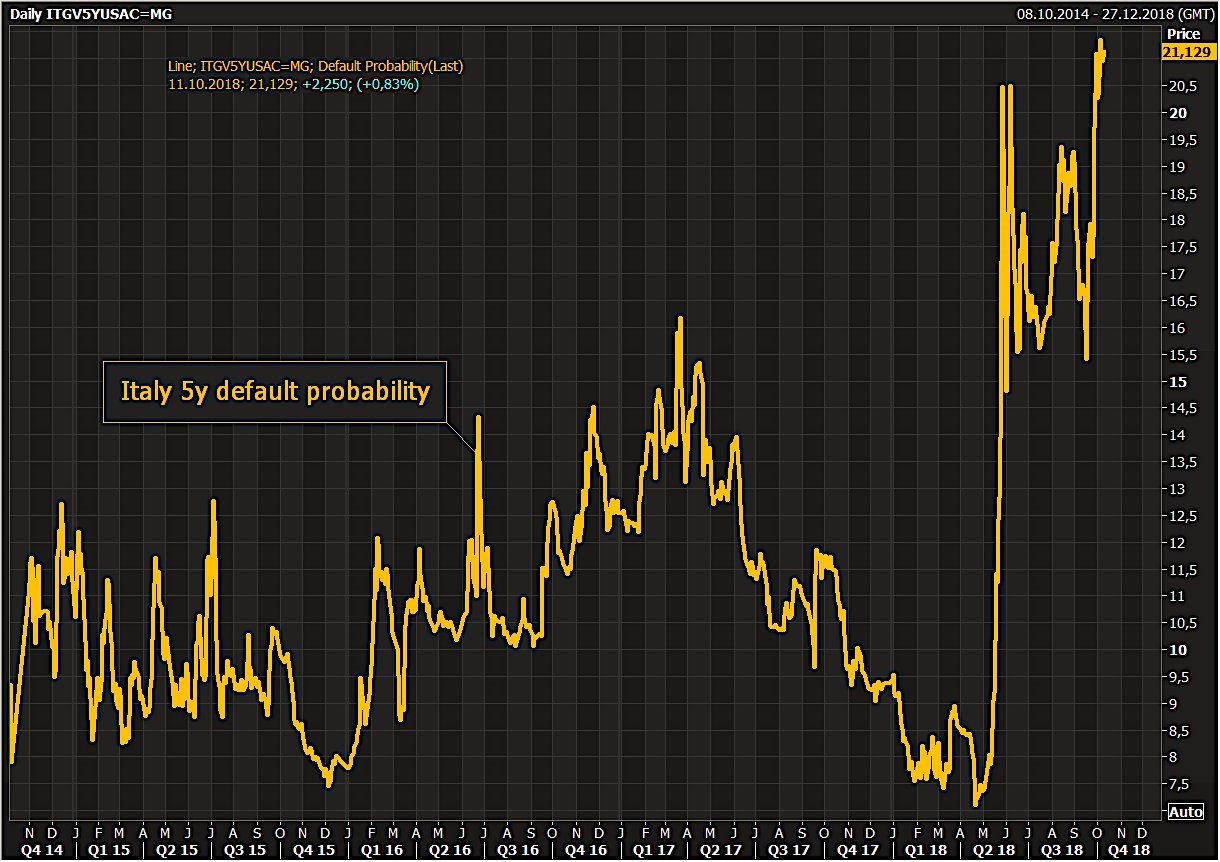

At the same time, the market is pricing the probability of an Italian default over the next five years at greater than 20%:

Source: Bloomberg

Source: Bloomberg

Meanwhile, in the US…

“I think the Fed is making a mistake. They are so tight. I think the Fed has gone crazy.”

– President Donald Trump, yesterday

We agree with the president. The Fed is crazy. However, this isn’t a recent development. The madness arrived a long time ago.

It’s worth remembering that during his election campaign, Trump claimed the Fed had blown a gigantic bubble in the stockmarket and created a false economy. But now he’s in charge, he can’t let the bubble burst on his watch. He’s got to give it more juice.

His remarks were made in response to the colossal “risk-off” move that began in the US stockmarket yesterday.

Across the pond, the Nasdaq 100 lost 4% of its value, its biggest drop in seven years. The fallout was wide – the Japanese Nikkei dropped soon after, causing its own dislocations, to the point where all major markets in Asia are down on the year.

It’s getting hairy out there. I think we’re close to the point where passive investing, and “buying the dip” ceases to be effective.

Something interesting to take away from the recent action is that stocks and bonds seem to be changing their relationship to one another. Market behaviour over the last 20 years has many investors base their portfolios on the premise that when stocks go down, high grade bonds go up, and vice versa. The reasoning goes that when stocks lose value, there will be a safety bid for bonds, and when inflation causes bonds to lose value, there will be an inflation bid for stocks.

You can think of this as a negative correlation between stocks and bonds, or a positive correlation between stocks and bond yields (which go up when bonds lose value). However you think about it, this strategy doesn’t work when both high grade bonds and stocks sell off at the same time. This occurred briefly during the “volmageddon” crash in February, and the correlations have once again begun to fray this week.

The last times this occurred over a sustained basis was 2005-2007, and 2013-2014 – both instances of course leading to severe pain for investors in stocks.

Until next time,

Boaz Shoshan

Editor, Southbank Investment Research

Category: Economics