My mum lives in front of the Wilder Kaiser. It’s a pretty mountain in Austria. The top half is a shiny face of bare rock which glows in the afternoon sun.

You can climb up and over through the Ellmau Tor. A few years ago, a Canadian friend and I made it much of the way up. But there was a particular obstacle I didn’t expect. Rubble.

It felt like climbing a sand dune at times. Every step’s foothold slipped down a few inches. You could smell the burnt smoke of flint as rocks the size of baseballs cascaded over each other and tumbled down the mountain.

The goats watching us thought it was hilarious, and let us know about it too.

Eventually, we settled on the view and decided we were high enough.

Britain’s retirees will do the same. For the same reason.

For every step you’ve taken up pension mountain, the ground has given way under your feet.

Not only that,

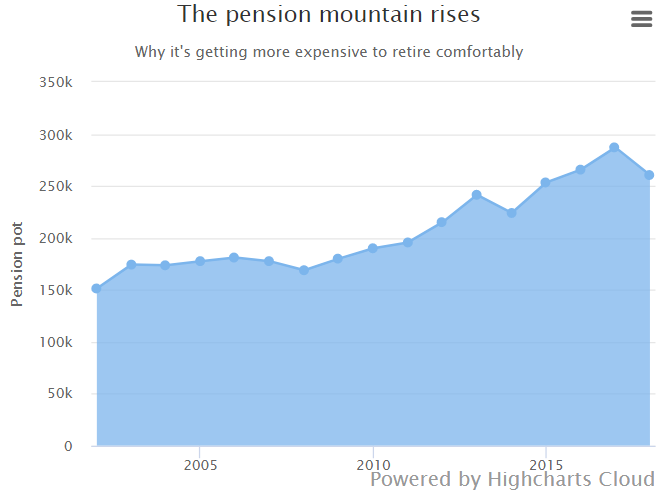

Pension mountain is growing faster than you can climb

The pension firm Royal London put on display how much money you need in your pension pot to retire comfortably. The calculation is based on what an annuity company will sell you an income stream for.

The figure is £260,000 for homeowners and £445,000 for renters. But it’s not the figure that’s the really important part here. The specific number varies wildly between people depending on their circumstances.

It’s how that figure has changed over time that needs emphasising. In just 18 years, it has almost doubled.

Source: Telegraph

Source: Telegraph

Keep in mind, this is to achieve the so-called comfortable retirement – £17,800 in income a year. It also assumes you’re eligible for the state pension as part of that income.

How are we doing when it comes to actually paying for our promises? Impressively badly, IPE explains:

Steve Webb, director of policy at Royal London and pensions minister during the period measured by the ONS, said the figures were “truly mind-boggling”.

“Today’s population has built up £7.6trn in pension promises but has only set aside about a third of that amount to pay for them,” Webb said. “The rest will have to be financed by tomorrow’s workers.”

Good luck pitching that to tomorrow’s workers. Especially with less of them per retiree each year the country ages.

Instead, the retirement age and the size of the state pension will have to change for the worse. Companies will have to put up with steadily increasing pension payouts, crippling their profitability. Which further cripples the returns of pension funds…

Are we making progress on fixing the problem? Nope, the Office for National Statistics reports the underfunding figure for all pension promises put together grew by a trillion pounds between 2010 and 2015.

So the amount you need to retire is growing fast. We have only secured about a third of our existing pension promises as a nation. And that gap is growing fast. The government is about to default on its share of the promises by changing state pension terms.

The mountain of rubble you have to scale sure is growing fast.

Let’s look at what’s gone wrong. And how it will go terribly wrong in the future.

Even if you think you’ve amassed easily enough to retire on, don’t bet on it. You’ll be affected as the system breaks down.

Escaping pension purgatory

Financial markets and central banks have robbed millions of people of a decent retirement. Democratic politics is practically designed to avoid fixing the problem.

It’s bad news all round. Let’s dig deeper, so you can identify what to do about it.

The aim of the modern pension system is to leverage investment markets’ magical ability to generate returns. The financial industry doesn’t believe its own disclaimer that “past returns are not a guarantee of future results”. Instead, it presumes markets will continue to rise rapidly forevermore… and we will all retire happily ever after.

The theory says that by investing your savings and generating returns of 7-8%, you’ll build up a big enough pension pot to then sell down in retirement.

The trouble is that markets don’t inherently return 7-8%. And that destroys the concept completely.

Lance Roberts from realinvestmentadvice.com calculated that for every percentage point less in returns that markets deliver, you need to add 10% in contributions to achieve the same pension pot. He estimates returns of 3-4% are more honest. So contributions would have to rise about 30%.

Perhaps that’s plausible for some. But the same principle returns on the way back down. Unless you buy an annuity, you only sell down the pension pot slowly in retirement. For the first few years, the bulk of your investments continue to provide returns.

Unless you hit a financial crash at the time… but those never occur in the pension calculations, so don’t worry about that…

Anyway, the problem of poor returns multiplies on both the way up, and on the way down.

At what level of returns and risk does the whole premise fall apart? If the FTSE were stuck below the level of its 2018 peak for 18 years, just theoretically of course, then why invest in it to grow your pension pot?

This is why many nations place their faith in bonds instead. These return interest and are far less volatile. It makes the whole system more predictable.

But central bankers have crushed interest rates. The return on bonds is now as pitiful as stocks in the UK.

Given the system clearly isn’t working, the government’s answer is the same as ever: give it more money.

Pension contributions under the opt-out system are set to boom in the UK. We’re moving towards the famous Australian system, which is called superannuation.

Unfortunately, that system was the worst performing one globally during the financial crisis of 2008… and the country didn’t even have a recession.

The lower returns of financial markets are a not a reason to increase your risk. They’re a reason to opt out and look elsewhere.

Especially if a crisis strikes.

Until next time,

Nick Hubble

Capital & Conflict

Related Articles:

- Opt out of the blunder from Down Under

- The pension panic is coming

- Why the European sovereign debt crisis is back

Category: Economics