My friend Tim Price is out with a warning. He’s spotted what he calls “the Third Crossing”.

Don’t worry, it’s nothing morbid or religious. Unless you’re praying for your retirement.

The last two crossings triggered the most memorable stockmarket crashes of our time. So you’ll never guess what Tim predicts the third time around…

You can find out just what has Tim so worried here. And, more importantly, what you should do about it too.

But there’s another similar crossing taking place with a more optimistic outlook. For one particular sector of the investment world, that is. (It’s pessimistic for stocks too…)

Have you noticed the lack of commodity news in the media lately? Commodities used to be a white-hot investment trend.

Just a few years ago, the media was so keen to interview commodity guru Jim Rogers that he’d go live from his exercise bike in his home gym. Between the huffing and puffing, Jim would spruik commodity investments as an antidote to central bank meddling. He’d explain his daughters are learning Chinese because of the coming voracious demand from consumers there.

These days, Rogers’s former investment partner George Soros gets all the attention with his political meddling instead. Commodities don’t get headlines at all. Mid-tier cryptocurrencies are more popular. The crypto-news section replaced the commodity news section on my Bloomberg homepage.

Small cap diggers and drillers used to offer the returns that cryptocurrencies do now. Discovering oil, gold or rare earth metals sent stocks soaring even faster than cryptocurrencies do today.

Well, the “crossing” I found today says the commodity investment sector is finally due for a comeback:

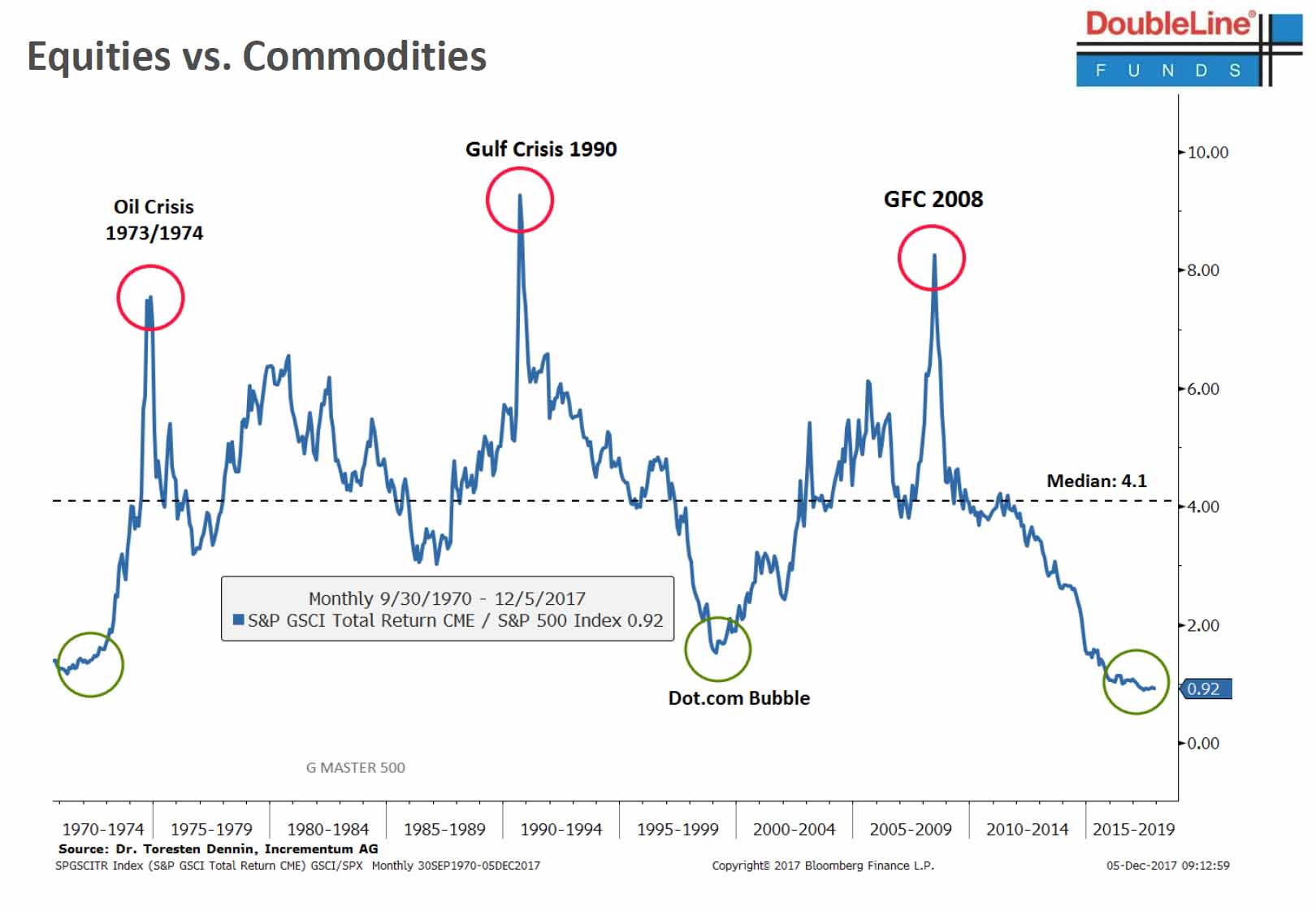

The chart is from Jeff Gundlach’s investment firm DoubleLine. Gundlach is famed for a series of successful predictions, including the election of one Donald Trump early in the campaign. His latest public prognostication is a good run in commodities.

The chart shows that commodities are terribly undervalued relative to equities. That means owning commodities should outperform equities in coming years.

“You go into these massive cycles,” he told CNBC. “The repetition of this is almost eerie. And so if you look at that chart the value in commodities is, historically, exactly where you want it to be a buy.”

The thing is, the chart also shows that crises tend to come along with the turning points. So we’re due for one.

Which commodities do well during crises? That’s easy. Tim Price explains in his report.

The question is what the crisis will be. If it’s going to end up being bullish for commodities, that gives you a hint. And you can try and learn from history too. The previous run-ups in commodity prices from extraordinary lows featured high inflation, rising oil prices, stockmarket bubbles and monetary meddling.

So what’ll it be this time around?

Could it be the implosion of the cryptocurrency bubble and a return to hard assets that drives the coming turning point?

Or perhaps a crash in the terribly overvalued FAANG stocks Facebook, Amazon, Apple, Netflix and Google? They’re the very opposite of commodity businesses.

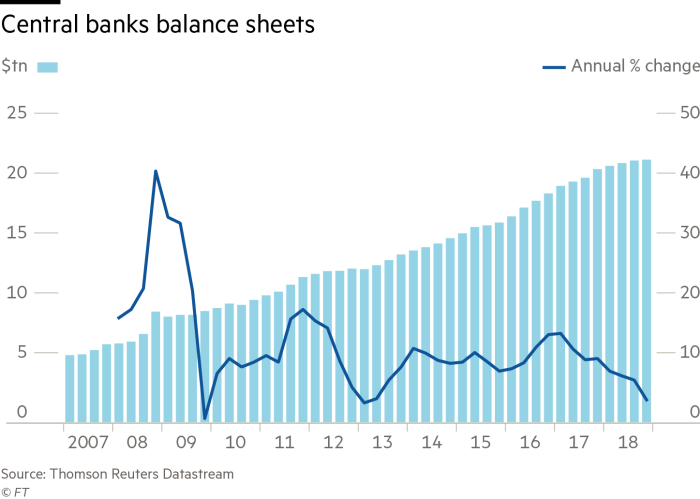

Perhaps the failure of funny money might be exposed as the sick economy gets weaned off the quantitative easing (QE) drug. Central bank balance sheet are set to stop growing next year…

Inflation in the UK just hit levels that force the Bank of England governor to write a letter to the government. Unemployment in the world’s major economies is extraordinarily low, priming more inflation. And the geopolitics of oil and gas are looking rather worrying in almost every major hub.

Whatever the crisis turns out to be, commodities look like a very good bet. But it’s far from safe.

The biggest risk to the thesis above is China. If China slows, so too does the commodity boom. Although, not necessarily for all commodities.

With numbers like these from Forbes you can see that China’s slowdown is not playing out yet:

China’s commodities imports rose in November after a seasonal fall in October due to holidays only. Imports of crude oil, copper, iron ore, natural gas and coal grew by 19%, 32%, 19%, 13% and 4% month over month, respectively.

Annualized, China’s appetite for fuel is strong. Crude oil and natural gas imports rose 15% and 42%, respectively.

Copper and iron ore imports grew almost 5% and 3% on the year, keeping iron ore futures high.

And China’s recent economic data for November shows plenty of strength too. Retail sales were up 10%, industrial production up 6% and fixed asset investment up 7% year on year.

Commodities are go, at least for now.

So…

How do you invest in commodities?

The good news is, it’s easy, fairly cheap and doesn’t involve piling copper wiring in your attic. In fact, the London Stock Exchange (LSE) now has an extraordinary range of listed securities which allow you to get exposure in exactly the way you want.

From specific bets on heating oil [LSE:HEAT] and natural gas [LSE:NGAS], to diversified bets within sectors like agriculture [LSE:AIGA], or just an all-in commodities ETF like [LSE:AIGC]. And many come in a pound or US dollar version if you want to add or take out currency risk. The major commodities have leveraged versions too, if you want to double the risk and returns.

The best list of commodity ETFs I could find was here. There’s even an ETF for Lean Hogs [LSE:HOGF] if you want to hedge the cost of my family’s Christmas lunch.

But be sure to check out Tim Price’s prediction before you decide what to buy.

Britain’s missing investors

It seems to be a day for charts and reversion to the mean in Capital & Conflict. The idea is that, if something is at its historical extremes, then it’ll snap back. And that creates an investment opportunity.

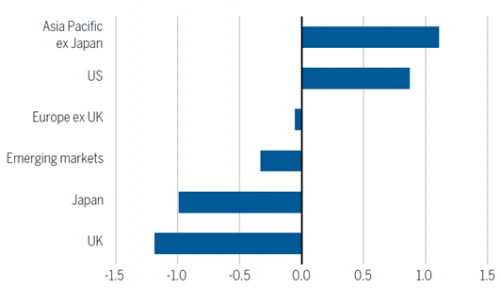

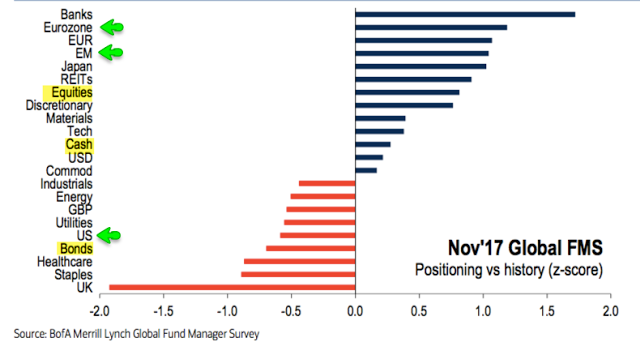

Well, according to these two charts, fund managers are massively underexposed to the UK stockmarket. That means they don’t own as many British stocks as they did historically.

Figure 1: Global Asset Allocators Significantly Underweight Japan (Z-Score in Standard Deviations from Mean)

Source: Wellington Management, November 2017. Data as of October 2017. Positions shown reflect positioning of funds in the EPFR Global universe versus their respective benchmarks.

Source: Wellington Management, November 2017. Data as of October 2017. Positions shown reflect positioning of funds in the EPFR Global universe versus their respective benchmarks.

First of all, a word of caution. In one chart, fund managers are overweight Japan and in the other they’re underweight. The data is for the same month, but covers different groups of funds. So the results here are not ironclad or universal. That’s why I included both to strengthen the argument about fund managers avoiding UK stocks.

Let’s assume there’s some truth to what they agree on. Fund managers are underweight UK stocks.

You’d think this is related to Brexit. Fund managers are hesitant to hold UK stocks as the pound gets into trouble and fragile trade ties get the UK into trouble.

Of course, European fund managers probably did a runner over the last few years. And others who owned stocks via the LSE instead of the dual listings on the Australian Securities Exchange (ASX), American markets and other places probably swapped over to the other exchanges too.

We looked into the outflow of foreign investors a while back in Capital & Conflict while refuting the Bank of England governor’s claim that the UK relies on the “kindness of strangers”.

Anyway, if you believe in reversion to the mean, then UK shares will see a lot of buying from funds around the world at some point.

Unfortunately all these measures are relative. They suggest it’s better to own UK stocks and commodities, but that doesn’t necessarily mean they’ll do well. Just better than foreign stocks.

In fact, the same sort of measure tells us that even the UK stockmarket will be struck down in a global crash soon. See if you agree.

Until next time,

Nick Hubble

Capital & Conflict

Related Articles:

Category: Economics