The fallout from the Nasdaq nuke on Wednesday persists across markets. Asian markets have had a bounce, but in the West, stocks are suffering. The FTSE, the S&P, and the EuroStoxx have continued to bleed.

And importantly, government bonds in the UK, America, and Europe are not providing shelter. Bond prices are continuing to fall, and yields are continuing to rise, despite the grief in the stockmarket.

We highlighted the fundamental risk this represents yesterday. The last times this occurred on a sustained basis was 2005-2007, and 2013-2014, which led to intense pain in the equity markets.

Should stocks and bonds continue to sell off at the same time, the age old premise (around which considerable regulation is based), that bonds are safe in a time of crisis will be shattered, and scarred investors will need to find sanctuary elsewhere. (Where? Tim Price knows just the place. But that’s only for subscribers to The Price Report.)

Of particular note with this dynamic are ‘risk-parity’ strategies. Risk-parity fund managers (most famously Ray Dalio) own stocks, but also use large amounts of leverage in bonds to match the returns and the volatility of those stocks. In times when stocks go down and bonds go up, and vice versa, this is hugely profitable. When that correlation breaks, it’s quite the opposite. Around £132 billion is invested in such strategies – a drop in the bucket in global markets, but significant nonetheless, especially considering the use of leverage.

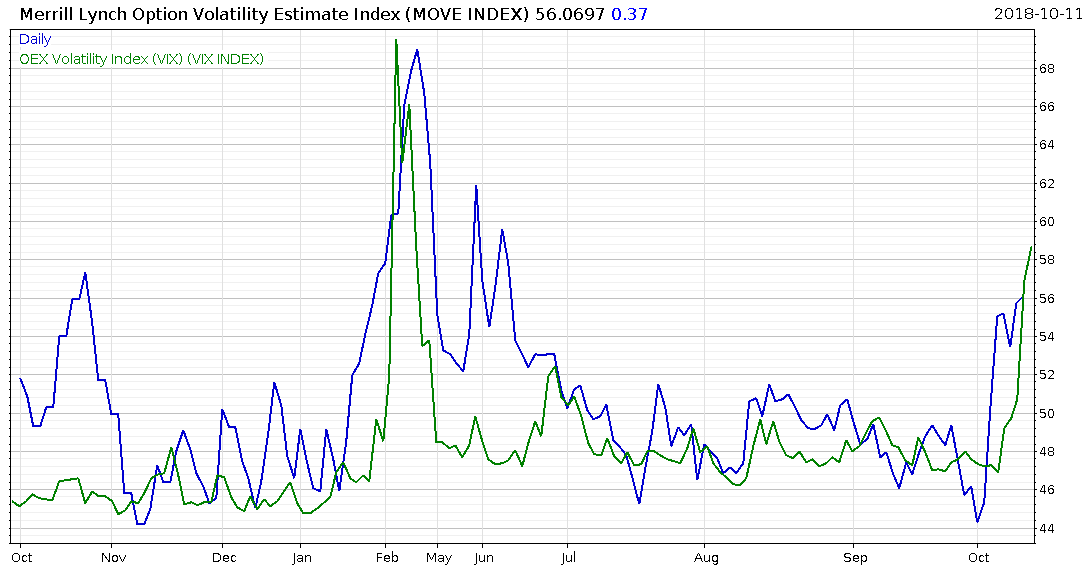

Insurance for both stocks and bonds is getting much more expensive, as measured by ‘implied volatility’ in the options market:

US implied stock market volatility in green, US implied bond market volatility in blue

But gold has caught a safe haven bid. The yellow metal is maintaining its status as a safe haven, despite not yielding a return in a higher rate environment. Should Bloody October continue as it has begun, gold will look even prettier in the future than it does already.

Speaking of which, Italian debt faces demotion in a few weeks. Standard and Poor’s and Moody’s, two of the ‘big three’ credit ratings agencies have Italy’s credit score up for review, with decisions to be made by the end of the month.

Should Italian debt be stripped of its investment grade rank, bond managers limited by mandate to only invest in investment grade bonds will be forced to sell, like it or not. Which will only make things worse for the Italian government, by forcing their cost of borrowing higher.

With the Italian deputy prime minister saying he will do ‘the exact opposite’ of whatever the EU demands of their budget, the degradation ceremony for Italy’s debt is right on schedule. Click here to find out what happens next.

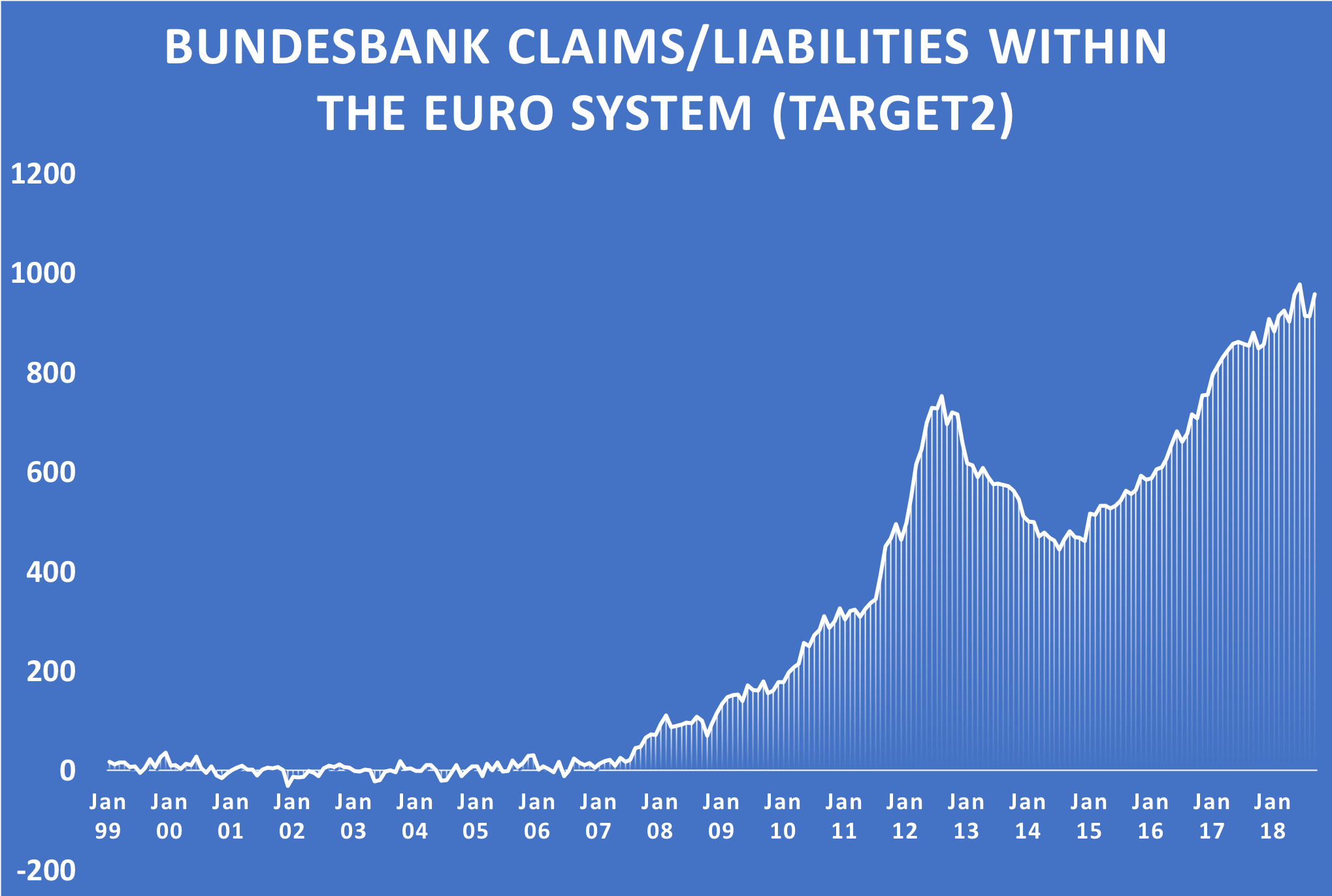

Elsewhere in the Eurozone, where Germany enjoys 10 year borrowing costs of only half a percent, the metric Alan Greenspan warned us of continues its inexorable march upwards:

By the way, if you’ve only just joined us here at Capital & Conflict, that line is supposed to linger around the zero mark, and not zoom up. These are Germany’s surpluses accrued from capital flight into German banks from stagnant Euro economies in the south. Those surpluses are now closing on €1 trillion. The Italian graph is a mirror image of this, with a mountain of liabilities rather than claims.

These surpluses and deficits were supposed to average out to zero over time, with all the Euro countries growing at the same speed, under one currency, and one central bank.

But this idea of European monetary harmony is a fantasy. And the sooner investors realise this, the better.

Have a great weekend!

Boaz Shoshan

Editor, Southbank Investment Research

Category: Economics