In the final death throes of the great commodity bear market of the 1980s and 1990s, a pound would buy you 2.65 Canadian dollars.

For the British, Canada really was a cheap country to visit.

But of late, it’s been anything but. My eyes have watered on recent trips to Toronto as I’ve reached for my wallet. Just last year, such was the pound’s weakness, that the exchange rate hit C$1.52.

But all that seems to be changing. It could be time to back the pound versus Canada’s currency again…

One of the biggest currency stories of 2014

I think the one of the currency market stories of 2014 – and one I should have mentioned in my predictions piece last week – is going to be the weakening Canadian dollar.

It’s been strong for so long, I was beginning to take it for granted. But I think this year is the year it gives.

Like the Chilean peso, the Aussie dollar, the Brazilian real or even, to an extent, the Norwegian krone, Canada’s currency tends to appreciate during periods of commodity strength, and weaken during periods of weakness.

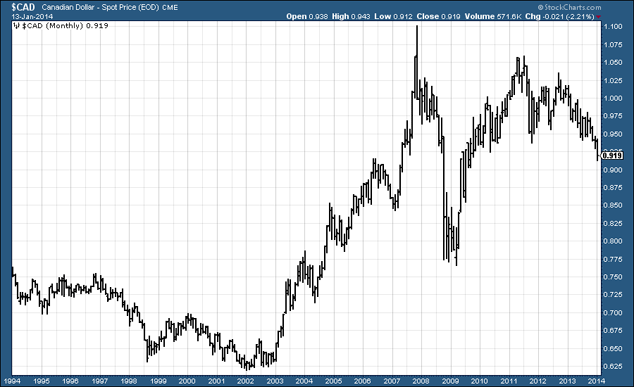

In early 2002, not far off the beginning of the great commodities bull market, the Canadian dollar could buy you just 62 US cents. Barely five years later, in late 2007, with many metals prices peaking, it was US$1.10. That’s not far off a double. In the context of national currencies, particularly for countries next door to each other, that’s extraordinary.

At the time, the US was experiencing its massive housing bust. I was at a conference in Toronto around about the time. I remember hearing overpaid Canadian mining executives, flush with cash and high-priced stock and options, laughing at the prices of the real estate they were able to buy next to the sea, lake or golf course.

They’re not laughing now. One of the last things they need – on top of all that they have been through in the mining bust that began in 2011 – is a weak currency.

Many of their mines are on foreign soil. Their input costs are denominated in foreign currency, but the money they raise is in weakening Canadian currency. Currently, a Canadian dollar will still buy you US$0.92, but the trend is very much down. The Canadian dollar is falling.

Below is a 20-year chart of the Canadian dollar versus the US dollar for your reference.

You can see the clear downtrend that has been in place since mid-2011 – a downtrend that is now accelerating. The words ‘cliff’ and ‘falling over’ spring to mind.

Mark Carney’s expert market timing

The Canadian dollar’s relationship with the pound – which, as someone with an interest in resource stocks, is of great concern to me – is also interesting.

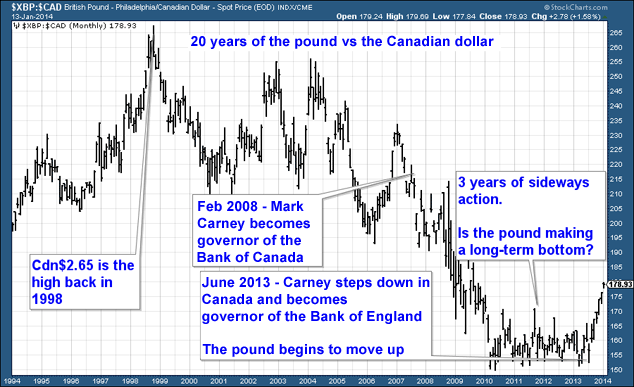

That C$2.65 peak I mentioned earlier in the pound against the Canadian dollar came way back in 1998. But the low – C$1.50 – came in 2010. That low was re-tested several times over a three-year period (2010-13) of sideways action – action that appears to be long-term bottoming action.

Unlike the US dollar, the pound was strong going into 2007 and weak coming out of it. As commodities have dawdled – their high was in 2011 – and finance has resumed its ascendency, the pound has risen and the Canadian dollar fallen. There is now a clear uptrend in place with a pound currently buying you C$1.78.

Of course, you can’t mention the currencies of the US and Canada without mentioning the man who has had a rather large role to play in the management of each – Mark Carney.

On the 20-year chart of the pound below, I’ve marked the point at which he became head of the Canadian central bank, and the point at which he stepped down and came over to the Bank of England.

It would be easy to look at the timetable and assume that Carney was responsible for the amazing strength in the Canadian dollar over the period from 2008 to 2011, as it broke to new highs.

And then he joined the BoE just in time for the pound to start looking up. The man’s got good timing, you have to say that for him – he’s a good trader.

Note – as the black line falls the Canadian dollar gets stronger and the pound gets weaker.

A bet on the pound is effectively a bet on finance, while a bet on the Canadian dollar is a bet on commodities. Given the action we’ve seen so far in January, I’d probably favour a bet on commodities over the next month or three – in other words the pound may weaken a little and the loonie strengthen. But the broader trend is very much in favour of the pound.

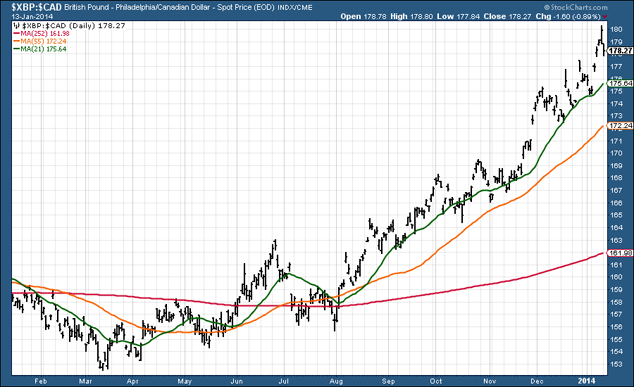

Below is a one-year chart. The price is trending up, the 21- and 55-day moving averages (green and yellow lines) as well as the one-year (red line) moving average are all sloping up and in alignment. This chart is a trend-follower’s dream.

Trends in forex have a habit of going on for many years (just look at the yen!). While I wouldn’t rule out a pull back to C$1.70, a move back to C$2 really doesn’t look so unlikely over the next eighteen months or so. Much depends on the success of the respective economies, of course.

What does this mean? Well, if you have money in Canadian resource stocks, you should think about hedging your currency risk. I can’t believe this long-time sterling bear is saying this, but a bet on the pound against the Canadian dollar looks a good one.

However, the implications for Canadian stock markets in general aren’t as clear-cut. Often when a currency falls, the stock market rises and vice versa – think Japan.

If you do decide you want to take a bet on the Canadian dollar versus the pound, spread betting is one of the easiest ways to do it, but just remember that it’s high-risk, and you can lose a lot more than your initial stake doing it. My colleague John Burford writes MoneyWeek Trader, a regular free email on the topic. Look to buy pullbacks.

• Life After The State by Dominic Frisby is available at Amazon. An audiobook version is available here.

• Follow @dominicfrisby on Twitter.

Category: Market updates